Politics is the art of using any situation to your advantage. A good politician is one who can extract maximum benefits, even from a crisis. And arguably, Trump is the best politician the US has seen since probably FDR. Love him or hate him - after 10 years in politics, having entered as a total outsider, he is the fiercest political force.

Currently, he must be asking himself one question - What do I stand to gain / lose if I end the war, vs what do I stand to gain / lose if I let the war continue?

The general assumption among analysts is that the cost of continuing the war far outweighs the benefit. From the economic implications to midterms, the conventional wisdom is clear. But is it true?

I spend my days reading and watching countless analyses. But from experts to armchair analysts, no one seems to have a proper understanding of the current situation. Forecasts lose accuracy in days, even hours. Explanations often fail to provide a complete rationale, as if the top geopolitical minds didn’t in fact have any idea what is going on.

Prediction markets’ sharps resorted to simple, generalist rationales in the face of enormous complexity; the war must end because the markets will eventually force Trump to sign a slop deal is the prevailing assessment.

What if there is a plan, however? No 5D chess type of plan that “plan trusters” pushed on us from day 1, but a plan that took shape as the initial strategic calculus failed? A ruthless calculation that yielded an uncomfortable result for most of the world, but one that offers potentially outsized benefits for the main actor, the US.

A Plan Was Born?

Today I will ask an uncomfortable question. I keep seeing signs and signals that defy a seemingly rational analysis. I don’t know yet where this journey will take me, but I want you to accompany me on it.

Conflicting Signals

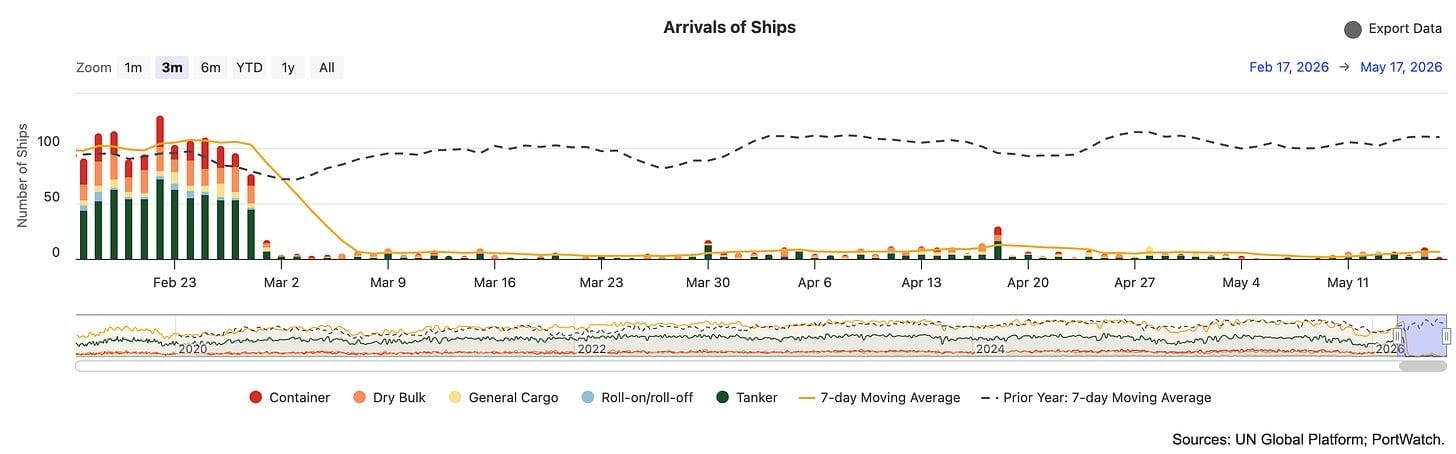

The recent developments don’t really make sense. Every day of the double blockade of the Strait of Hormuz brings enormous pain to the global economy. And yet Trump does little to change the situation. The US has been slow to try to break the Iranian blockade. When they finally tried to do something, it was quickly seen as a failure.

The Operation Project Freedom, announced as an escort operation, had been immediately downgraded to a simple advice and assistance project. The US Navy’s incursion into the Persian Gulf was met with an Iranian escalation. Seemingly a perfect casus beli to restart the war, but the US backed away from answering with fire.

The deals we see being announced don’t really show signs of progress. The wording differs; sometimes it is softer, but the underlying demands hardly move. Additionally, by introducing the closure of Iran’s ports, the US only tightened the overall blockade, preventing Iranian oil from hitting the already starved-for-energy markets.

I called it the most expensive game of chicken ever played. It seems, though, that the US does not intend to blink at all. If it did, we would see some signs, eg.:

- A concentrated effort to break the Iranian blockade.

- Deal proposals getting materially softer on American demands.

- Limited strikes on oil infra / decapitation strikes on key IRGC figures that oppose the current deal, especially after Iran hit the UAE.

- Increasing US assets and troops in the region (the current airlift operation is logistics to maintain the current force, not an increase in assets as some say).

On the other hand, we see other signs that run counter to the conventional wisdom:

- The US is actively plugging the oil & gas supply gap resulting from the SOH closure (extending the global runway).

- The Trump admin is actively coercing Canada through the Alberta separatist movement ahead of the USMCA renegotiation (presumably pushing big American demands behind closed doors).

- Venezuela is exporting more and more oil as Trump is forcing the US oil industry to invest in the country (extending the global runway).

- Trump is once again active in the Ukraine x Russia peace process, getting a 3-day ceasefire as an example (potentially forcing peace to unlock Russian energy).

- The Treasury and the Fed are actively negotiating new swap lines (and getting what they want in return).

- The Clarity Act is being forced through Congress (unlocking wider stablecoin use).

Additionally, we have some hard truths we need to face:

- The damage to the oil infra in the Gulf region is significant and irreversible in the short to medium-term.

- The political cost of a weak deal is huge and it’s increasing with each day of the stalemate.

- Iran feels too strong to fold to a deal that does not improve their position in the region and the world.

I’ve already highlighted how these 3 hard truths impact the short-term negotiations dynamics. However, I refused to look ahead as no solution made sense to me. Until now. It’s time to explore whether a long-term stalemate is in fact the optimal strategy for the US.

The Global Rupture

It is undeniable that the long-term closure of the Strait of Hormuz will completely derail the current supply chains and, with that, the global economy. But it seems that at the end of that dark tunnel, there is a future in which the US position is significantly improved.

It is hardly a perfect scenario. In fact, I doubt the war planners had it in mind when they started the conflict. They’d rather the war ended in a few days with a new regime in Iran. But since the reality didn’t go according to the plan, the plan needs to adapt.

Facing no good alternative, let’s see how a prolonged closure of the Strait of Hormuz can benefit the US. If we distill the issue enough, we have 2 main dimensions of the problem:

- The oil & gas supply.

- The monetary implications.

The consensus of experts is clear - the supply gap is impossible to bridge and the resulting crisis will affect every country in the world. But what if it is wrong?

Oil & Gas

Over 20 million barrels of oil per day transited the Strait of Hormuz before the war. The strait is now closed, but oil still flows through the East-West Pipeline in Saudi Arabia and we still have limited exports through the Fujairah port. In total they handle around 6 million barrels per day, leaving us with a 14.5 million barrels per day shortage.

Additionally, the gas shortage is estimated at 300 million cubic meters per day (ca. 10 billion cubic feet per day), representing ca. 20% of global LNG trade, but only 3% of the global gas supply.

The key question to answer here is how much of the gap can be bridged.

Based on my research, oil presents the biggest hurdle. If we consider the US, Canada, Mexico and Venezuela, they can provide an additional 3.5 million barrels per day in the short term.

The gas situation is more optimistic. The US can provide up to 3 billion cubic feet per day. When we include Canada, the number goes up to 5 billion.

However, in both scenarios, the situation changes when we include Russia in the equation, especially when it comes to gas. For oil, the increase is modest, with all the countries being able to provide a total of 4.5 million barrels per day. With gas, Russia can bridge the remaining gap, fully alleviating the situation.

That being said, we would need a permanent peace deal in the Ukraine war for Russian energy to be easily available for the global economy.

Russia

We know that Trump has discussed energy cooperation with Putin during his conversations with him. But any plan that includes Russia faces significant difficulties:

- A permanent peace in Ukraine.

- Oil shortage would still be equal to 10% of global demand.

- Russia would need to agree to stop selling oil to China.

Outside of the mere difficulty of ending the Ukraine war in such a short time, this solution wouldn’t really solve the oil issue. Even if Russia agrees to stop selling oil to China, it would only add 2 million barrels per day to bridge the gap, getting the total gap down to 8 million barrels per day, or 7.5% of global demand. If we add to it a coordinated release from various strategic petroleum reserves, we could bridge the gap down to 5-6 million barrels per day, or 4.7-5.7% of global oil demand.

This is probably the weakest part of this theoretical plan. Even in the best possible case, the world cannot avoid a massive oil supply shock. Demand destruction is unavoidable. The scale of it will be in the range of 5-10 million barrels per day.

Who Will Take The Pain?

Plan trusters are correct in one regard. Asia, and China specifically, will bear the majority of the pain from the Strait of Hormuz closure. Thus, I need to assume that Asian economies will suffer the better part of the overall demand destruction.

If we consider that Japan, South Korea and India will get priority treatment from the US and allies, the burden will be put on China and SEA.

A 5-10% supply shock coming at a region where most of the world’s manufacturing happens can wreck havoc on the global economy. But for the sake of the argument, let’s say that the oil flows would be redistributed as such to avoid a total catastrophe, eg. a collapse of a country. It’s an optimistic assessment, but not impossible.

The Bull Case

The argument I’m deriving from what plan trusters say and post is simple. The pain for the US is minimal to none, and in fact the US can benefit from the Strait of Hormuz closure in a short to medium-term.

The first leg of their argument is energy. America becoming the main energy exporter is a clear benefit they highlight. The second leg is financial.

Make America Great Again

The allure of the plan trusters is that their core argument is aligned with the wider MAGA ideology. The America First policy aims to bring jobs back to the US. It aims to revive American industrial power. Becoming the biggest energy exporter is surely a great step towards this goal. But it’s hardly enough.

The AI narrative and a massive data center expansion also serves that goal. But to truly enable America to grow a massive amount of investment must happen. We are talking trillions of dollars. This is an investment that the markets would be wary to make. After all, it’s low margin, capital intensive and time consuming. However, from a policy point of view, it is crucial.

We’ve already seen that Trump is not afraid to use statecraft to push this investment. He’s been touring the Middle East looking for investments. He forced TSMC to invest in a brand new fab in the US. He directed the Treasury to invest in Intel. He sees the role for the government in the economic transition for the US.

At the same time, there are hard constraints on what the US as a government can do. The main one is an appetite for the US debt. For years now the Treasury has struggled to finance the US government on long timeframes. The majority of the debt is rolled over using Treasury bills and short-term notes rather than 10 or 20-year notes. The problem here is twofold:

- Financing long-term projects with short-term debt poses a duration risk.

- Relying on bills and short-term notes requires the Treasury to ensure there is constant (or even increasing) demand for the short-term US debt.

But how does everything here fit into the Iran war strategy? In theory, there are 2 instruments the US government can use to improve its position thanks to the Iran war crisis - top-down and bottom-up.

Swap Lines

Swap lines are a top-down instrument. They are essentially a short-term debt that the Fed or Treasury can give to a foreign central bank. The foreign central bank, in need to liquid US dollars, can lend these dollars from the Fed / Treasury and put its own currency as a collateral.

Since eurodollar is the primary global currency, foreign entities, and thus central banks, have a constant need for liquid USD. In times of a crunch (eg. an energy supply shock), there are only 2 ways to get the dollars:

- Sell US assets (mainly debt) in possession of the foreign central bank.

- Take a currency loan.

The first option is sub-optimal for both the US and a foreign central bank. Selling US assets can create a slight, short-term distress in the given asset. Given that the US is looking to issue more debt, not less, it can create unnecessary turbulence in the debt market. Additionally, a foreign entity can only sell these assets once. After that we are back to square one, but with no US assets.

Such a scenario can create a death spiral. A world, in constant need of USD, violently shuts down international trade due to lack of the USD. The alternative is the swap line.

You can say it creates dollars out of thin air, and you’d be partly true. The full truth is that it’s the foreign entity (a central bank) creating its own currency out of thin air to post it as collateral. In that sense, a swap line is a vote of confidence from the US that the country is good on their promise. The ECB has had such a swap line since the GFC and the Euro debt crisis. So do the BOJ, SNB, the Bank of Canada and the BoE.

Swap lines are a bit more complex, but for the sake of clarity let’s not expand this paragraph by all the other swap lines in existence. Source: Council on Foreign Relations

But it doesn’t come for free. The European central banks got the lines because the US and European economies are intricately connected. So are the Canadian and Japanese economies, with Japan also being the most important Asian ally. Any other country looking to get the swap line would need to give something in return.

Let’s have a recent example of the UAE. It’s been a staunch ally of the US in the region. It signed Abraham Accords. It promised to invest billions in the US. It willfully went through daily strikes on its territory during the kinetic phase of the Iran war. And it left OPEC. Quite a pack of gifts if you ask me.

In our scenario, an energy supply shock will create an environment of economic difficulties. Countries that are most exposed to the crisis, will start to experience capital outflows. Their currencies will depreciate, creating a death spiral strong enough to collapse the economy of a country.

India, Indonesia, the Philippines and other, smaller SEA countries will face these issues in the coming weeks. In order to protect their currencies, and their economies, they will come to the US to get a swap line (just like Argentina did recently). The US will be happy to give them, on certain conditions.

This way, the US can create a team of allied nations. These nations will be forced to cooperate and deeply entangled. Allies by necessity, but still allies.

Stablecoins

But what happens if there is no swap line? Let’s take a look at Nigeria. The country has a structural mismatch in its economy: there is a high demand for foreign goods, but the country lacks any serious export goods to bring in foreign currency. Nigeria has vast oil reserves, but lacks the infrastructure to extract and process it.

The resulting problem is a constant shortage of US dollars. Since the mismatch is structural, there is little Nigeria can do to fix the issue. The outcome is simple - there are periodical dollar shortages that result either in a massive currency depreciation or an artificial currency peg. Ultimately, both cases end in a loss of trust in the Nigerian Naira and the economy running mostly on scarce dollars. In the first case the dollars are accessible on the open market, but expensive. In the second case privileged entities get access to cheap dollars, while the rest are forced to acquire dollars on a black market.

In neither case though there is a clear benefit for the US. The de facto dollarization of the economy gives no upside to America. The situation changes when the individuals and entities are encouraged to use stablecoin dollars instead.

Stablecoins, as presented in the Genius and Clarity Act, need to be fully collateralized by Treasury Bills. If the de facto dollarized economies used USDT (USD Token), they’d create demand for US T-bills.

Usually it’s the elites of a country that reap the most of the upside from a troubled economy. Their access results in wealth extraction. If the access to dollars is democratized through the stablecoins, the benefactor of the wealth extraction is the US government through new demand for T-bills.

Conclusion

High-level, the playbook is simple:

- Create a global energy crisis.

- Position yourself as the main energy exporter.

- Control energy flows.

- Force the main troubled economies to invest in the US in return for the swap lines and energy contracts.

- Participate in the wealth extraction from all the other distressed economies through stablecoins.

The end result? A booming domestic energy industry combined with plenty of investment money to revive the American industrial power. What can go wrong, huh?

The Bear Case

There is one problem with this thesis. Goods don’t self-appear in stores. The real economy does not run on dollars. It runs on supply chains. It runs on work being done, from the very upstream of mining to the last mile delivery of your new iPhone. The US can have all the money in the world. It won’t matter though if there’s nothing to buy.

The bear case for the plan is simple. The global supply chains are a complex system. You can introduce some chaos into a complex system and most of the time everything will work out fine somehow. But there is a threshold after which it all falls apart. We are dangerously close to this threshold.

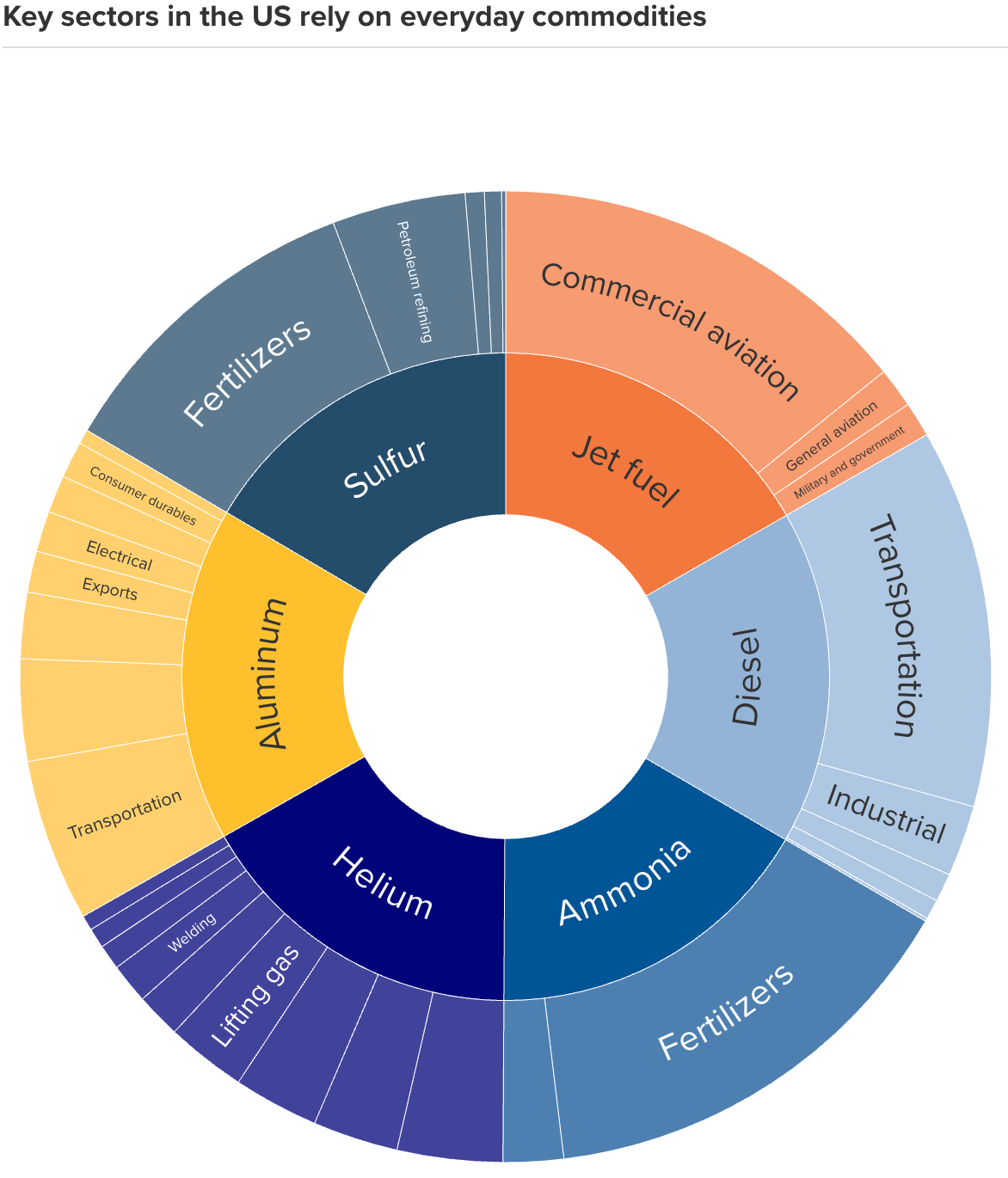

The Strait of Hormuz is arguably the most important waterway in the world handling:

- 20% of global oil supply.

- 20% of LNG trade.

- Up to 50% of global urea demand.

- Up to 35% of global fertilizer demand.

- 50% of seaborne sulfur trade.

- 33% of global helium production.

- 9% of global aluminum demand.

Are these gaps bridgeable? In isolation, maybe. But in their totality, there are cascading effects. A combined energy, food and manufacturing stress can collapse the complex system of international trade. The thing is, we have no idea when it will happen. It might happen today, tomorrow or several months from now. To be honest, it might already be too late.

The US might be mostly self-reliant on energy, fertilizer and helium. But when it comes to sulfur, not so much, as roughly 30% of supply is imported. It imports up to 80% of aluminum. But we’re barely scratching the surface.

Helium is needed for specialized semiconductors production. The US is unable to supply enough helium to Asia to sustain this production and has no domestic production yet. Fertilizer shortage will result in a massive food shortage globally. Sulfur is not only used for fertilizers, it is also used for eg. rubber vulcanization.

You could write a whole book about the complexity and interconnectedness of the global economy and it wouldn’t be enough. The core point here though is that the US cannot escape adverse effects of the Strait of Hormuz closure. Sure, they will appear further down the line, but they will. The silver lining is that any other country will be even worse off.

The bear case for the scenario assumes that Trump and his advisors are aware of this.

Bull vs Bear

The bear case is an inevitable reality. The bull case is a plan along the lines of “you can’t let a good crisis go to waste”. As these 2 clash, there are realistically 3 options Trump has:

- Play the game of chicken and reap the energy and monetary benefits in the face of the bear case.

- See the bear case as too strong and thus:

- Escalate to remove the problem.

- Sign a slop deal to save face.

All the while, the IRGC is highly motivated and ideological. They are fighting their holy war and they’d be happy to dance to the tune of the global economy collapsing if it means defeating the big satan.

It’s Trump’s Bay of Pigs moment. His instincts are surely telling him to sign a slop deal and move on. But the Iranians are making it impossible, demanding more than what was in the JCPOA. At the same time, it is also what the core MAGA ideologues want. In that regard, they should be aligned with the tech and industry elites, who just want to see their wealth grow.

Other MAGA ideologues will want to go with the scenario. The rise of the US industrial power, the focus on the Western Hemisphere, the wider America First ideology; they all require an almost total decoupling of the global supply chains. America changing from the main consumer of the world to the top producer of the world requires a complete reorganization of global trade.

Usually, such a change takes decades to complete. However, a global crisis, although painful initially, can help usher in a quicker change. Thus the other MAGA wing can surely see the Iran war as the ultimate, final war in the Middle East. They can use it to advance their goals and if the world burns in the process, so be it. No American life would be lost in a double blockade scenario continuing for the foreseeable future.

Lastly, I see the Pentagon and parts of the deep state wanting a full invasion of Iran. After Iraq and Afghanistan, it would be the ultimate military project in the Middle East. Years of war, equipment orders for the MIC, Iran reconstruction possibilities down the line and the eventual takeover of the oil-rich regional power.

What Will Trump Do?

The last thing Trump wants is a new forever war that entangles the US far away from home, drains resources and breaks his main campaign promise. A full invasion of Iran would be the last resort. I see Trump signing the ultimate slop deal before he puts boots on the ground. Trump sees war as a tool in negotiations, not as a goal in itself. He vastly prefers the quick n’ easy, Venezuela style approach.

As you see, despite my utmost hate for the scenario I just described, I seem to fall back on it as the only viable way forward. Boots on the ground are a big no. So is a slop deal, as there is Israel and internal stakeholders who would do everything they can to break it. Thus we are left with what we have now: a perpetual negotiations roller-coaster with a double blockade in place.

Cornered, Trump seems to fall back on playing the game of chicken and periodically checking in on Iran to see if they are ready to compromise / surrender. He will try to get the small wins through swap lines, energy contracts, promises to invest in America and growing utilization of stablecoins. The plan trusters significantly overestimate the positive impact of the energy and monetary implications, in my opinion. But they are there.

If mine and the CIA’s analysis is correct, Iran has months before it starts to feel the real pain from the American blockade. And any decapitation strikes wouldn’t change that calculus. Additionally, they risk an asymmetric escalation from Iran, targeting Gulf oil infra, undersea internet cables, Bab-el-Mandeb Strait and more.

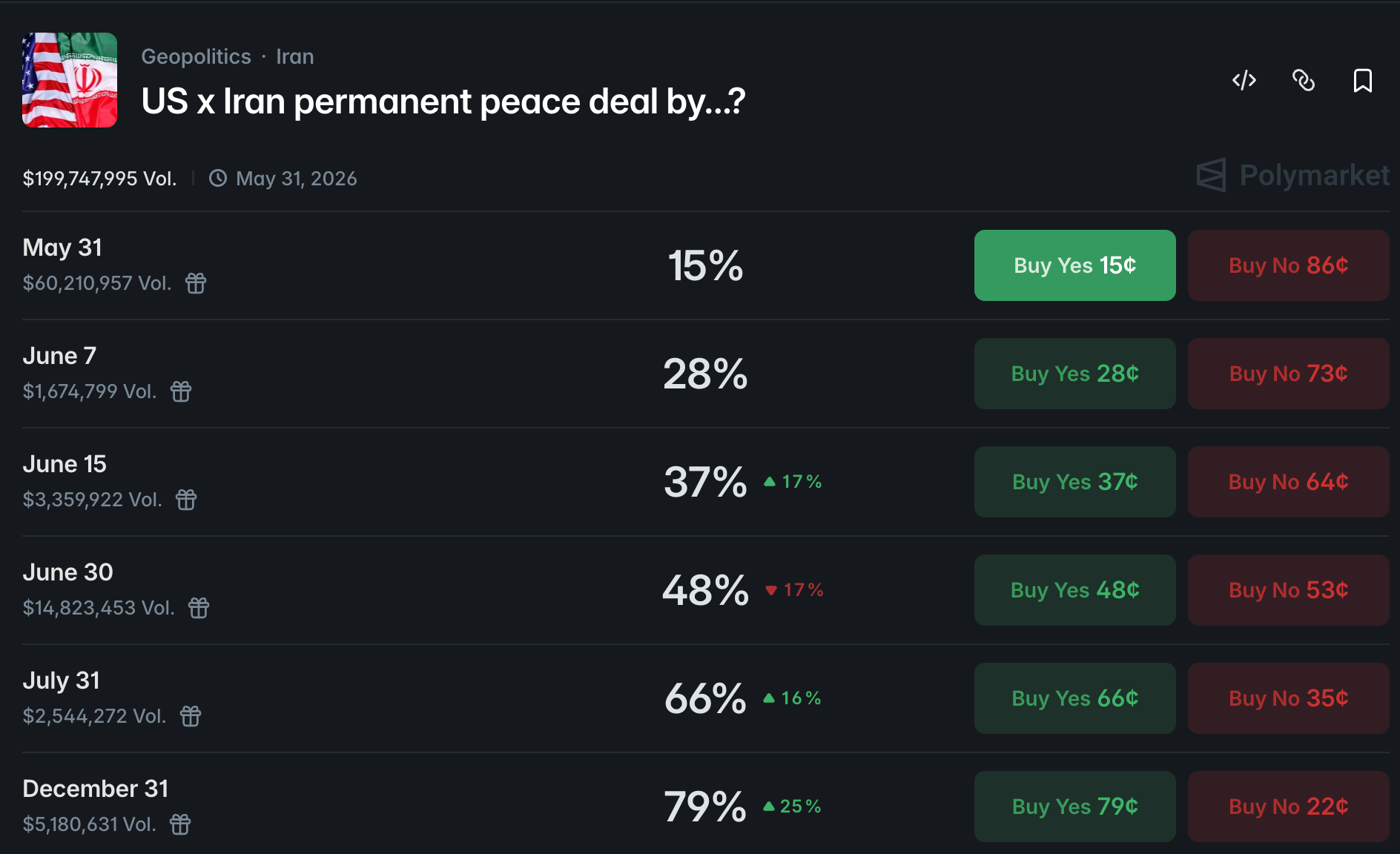

Prediction Markets

With everything above in mind, I have a rough approximation of my fair value by the end of June:

- Peace: 27%.

- Stalemate: 53%.

- Escalation: 20%.

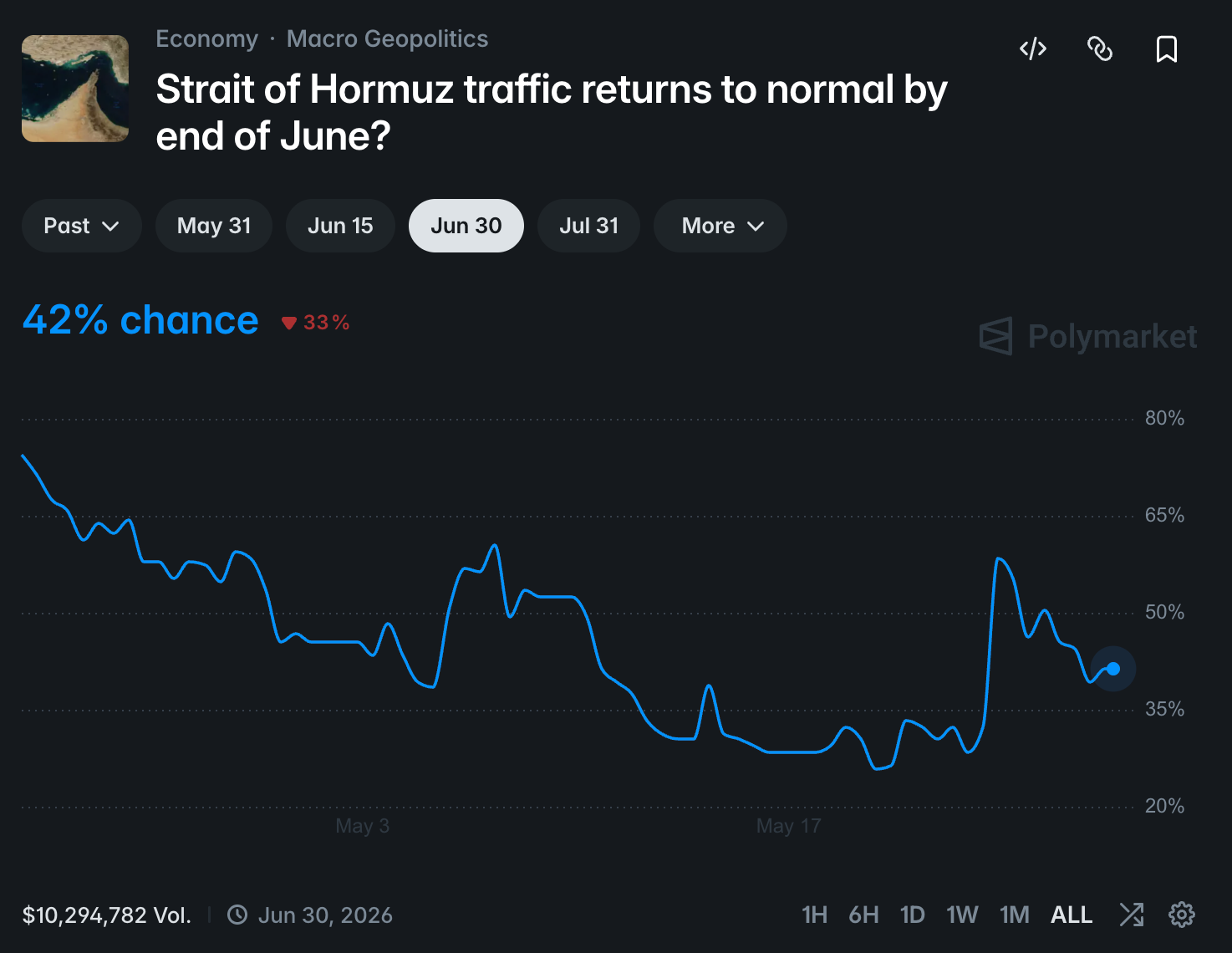

The double blockade continuing is the base case. Looking at the markets:

The recent negotiations narrative pushed the end of June peace price above my FV assessment. However, it is not enough for me to go on No. I’ll remain on the sidelines here for now.

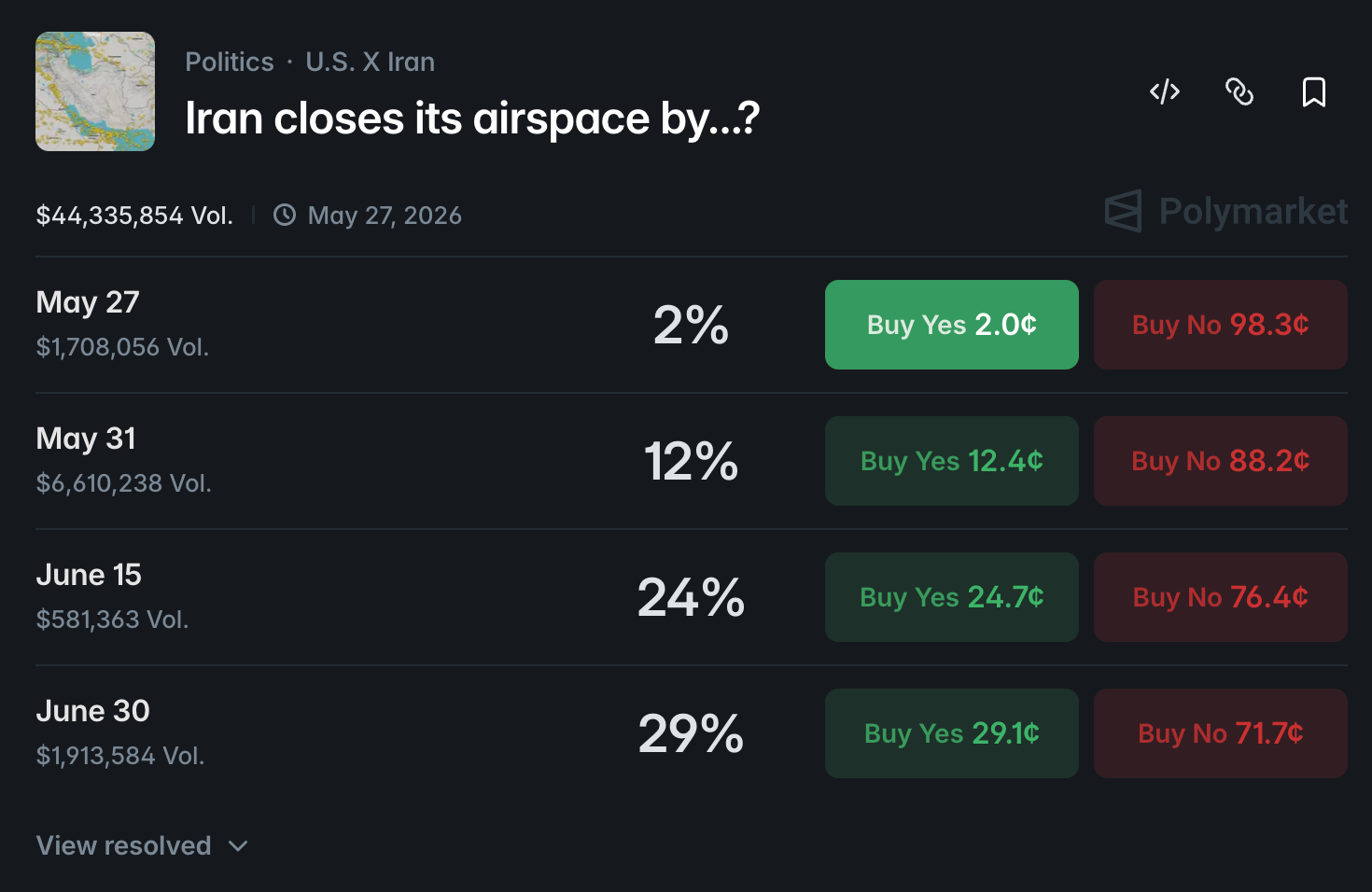

Here I think that the market is severely overestimating the chances for another round of escalation. Sure, there is a risk of the airspace closure without another kinetic round (it happened in January as Iran grew increasingly worried of an imminent strike) so I am conscious of my exposure. But I have a couple of positions on different strikes on No.

The Strait of Hormuz will remain closed in case of a stalemate and an escalation. The combined fair value of that is 73%. However, even in case of a peace deal, traffic normalization is not a given. It depends on the timing of the deal (the sooner, the better), the terms and the behavior of insurance companies and operators. I’m on No here on a couple of strikes.

The diplomatic meeting market is still a lottery. I don’t believe anyone can accurately price one as it can happen as part of the negotiations roller-coaster. I’ll be trying to enter the short-term market on the Yes side if I see the narrative taking us in the direction of a meeting.

What Would Need To Happen To Change The Calculus?

There are several catalysts that can change the current base case of a continuing stalemate:

- Iran starts to feel the pain faster. In case it happens, we shall see the chances for peace increase. On the ground, we should see a diplomatic meeting and a softening of the Iranian demands.

- There appears to be a sudden appetite for war in America. A large-scale terrorist attack. A serious assassination attempt. Generally, a big event is needed to change the public perception of the war. Then, escalation and invasion chances rise significantly.

- The Iranian protocol for crossing the strait starts to get regularly utilized by various countries paying the toll. This makes the US blockade moot (as I explained in my previous articles, the main pain for Iran, resulting from the blockade, is lack of access to a foreign currency; this problem is solved if they get the toll) and significantly extends the runway Iran has thanks to a steady influx of foreign currency. With the American leverage denied, strikes would be back on the table to reset the calculus and enforce the closure of the SOH.

- Trump loses the ability to threaten war due to eg. a Senate vote. In that case a quick deal is significantly more likely as Congress would essentially force an end to the war.

Wrap up

That’s all for today. It’s a funny moment when a rational analysis leads me to an irrational conclusion, but here we are. As it stands today, a prolonged stalemate is my base case. I have also identified the signals that would tell me the strategic calculus is shifting. They can appear today, next week or next month. Until then, we wait.

Stay strong and see you soon!